Key Takeaways

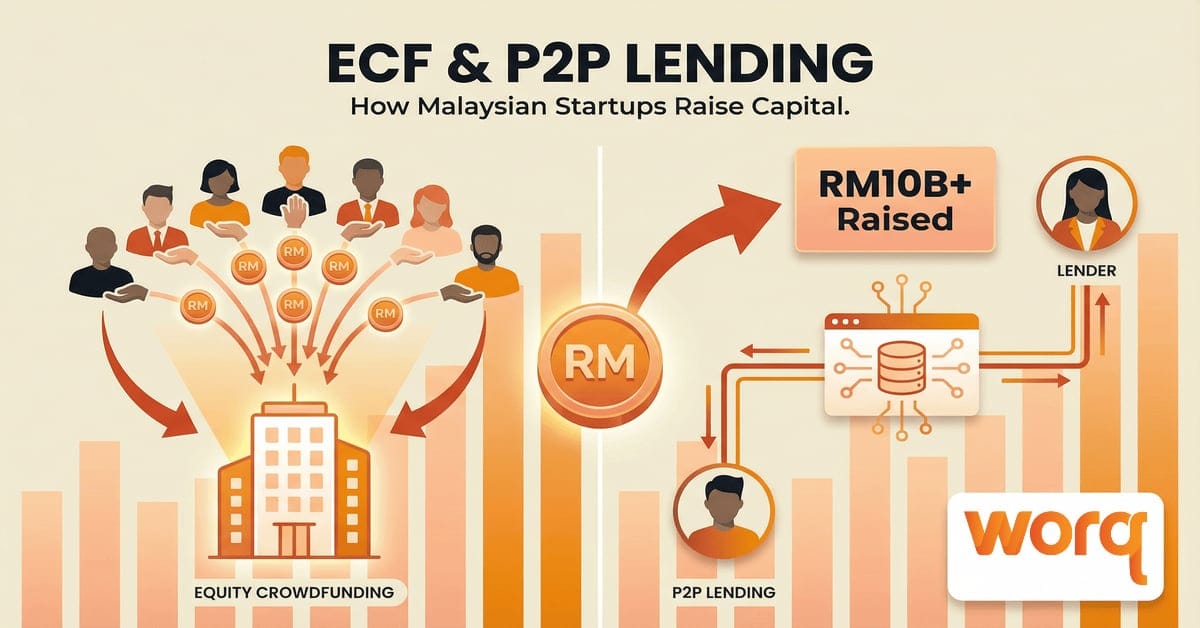

- Equity crowdfunding (ECF) and peer-to-peer (P2P) lending are two SC-regulated alternative funding channels in Malaysia that have collectively raised over RM10 billion for more than 23,000 businesses as of mid-2025, with 10 registered ECF platforms and 16 licensed P2P platforms currently operating.

- The NIMP 2030 CoSIF, launched in February 2025 with RM131.5 million, channels government co-investment directly through approved ECF and P2P platforms for startups in strategic manufacturing sectors.

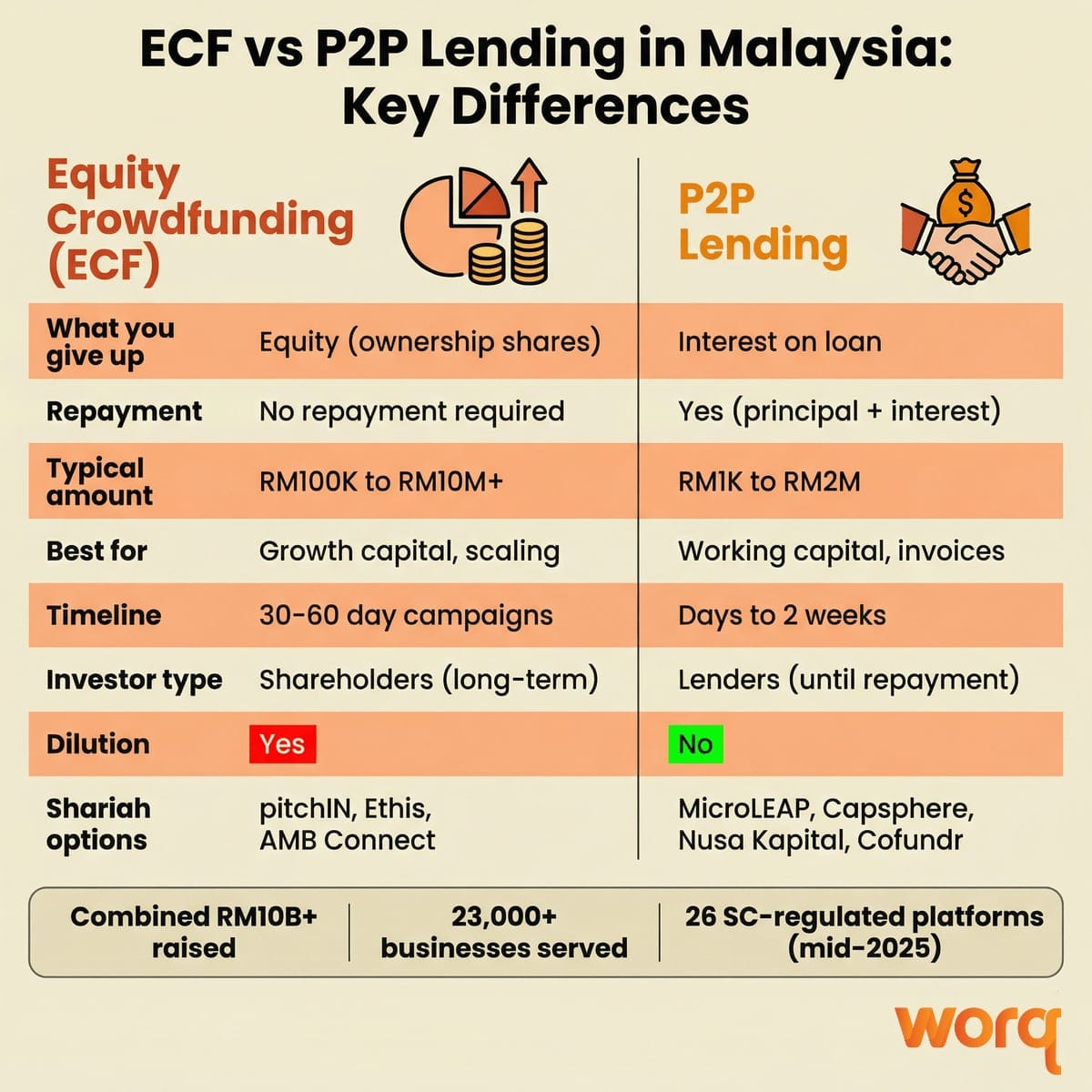

- Shariah-compliant options are available on both sides: pitchIN, Ethis, and AMB Connect for ECF, and MicroLEAP, Capsphere, P2P Nusa Kapital, and Cofundr for P2P financing.

- ECF suits startups seeking growth capital (up to RM20 million lifetime) with an investor community, while P2P lending suits businesses that need working capital quickly without giving up equity. Many founders use both.

Equity crowdfunding in Malaysia gives startups a regulated path to raise capital from hundreds of investors through online platforms. Paired with peer-to-peer (P2P) lending, these two alternative channels have collectively raised over RM10 billion and served more than 23,000 businesses as of mid-2025.

Malaysia was the first country in Asia-Pacific to regulate equity crowdfunding when the Securities Commission (SC) released its ECF framework in 2015. The P2P financing framework followed in 2016. Today, 10 registered ECF platforms and 16 licensed P2P platforms operate under SC oversight. And since February 2025, a new government co-investment fund called NIMP CoSIF channels RM131.5 million directly through these platforms, giving startups in manufacturing sectors an extra funding boost.

This guide covers how both channels work, the active platforms available, Shariah-compliant options, the CoSIF co-investment opportunity, and how to decide which channel fits your startup. For a full overview of every funding option available to Malaysian founders, start with our pillar guide on startup funding in Malaysia.

Table of Contents

- What Is Equity Crowdfunding (ECF)

- SC-Registered ECF Platforms in Malaysia (7 Active Platforms)

- What Is Peer-to-Peer (P2P) Lending

- Licensed P2P Platforms in Malaysia (6 Active Platforms)

- ECF vs P2P Lending: Which Is Right for Your Startup

- NIMP CoSIF: RM131.5 Million Government Co-Investment Through ECF and P2P

- Shariah-Compliant ECF and P2P Options in Malaysia

- How to Prepare for an ECF Campaign in 5 Steps

- How to Apply for P2P Lending in Malaysia

- Risks and Default Rates: What Founders Should Know

- Where ECF and P2P Fit in Your Funding Strategy

- Grow Your Startup at WORQ

- Frequently Asked Questions

What Is Equity Crowdfunding (ECF)?

Key ECF Rules and Investor Limits in Malaysia

- Lifetime fundraising cap: An issuer can raise a maximum of RM20 million in total through ECF platforms, excluding the issuer’s own capital contributions and private placements.

- Eligible entities: Only locally incorporated private companies (excluding exempt private companies) and limited-liability partnerships can raise funds through ECF.

- Investor categories and limits: The SC divides investors into three categories with different annual investment caps:

| Investor Category | Annual Investment Limit | Notes |

|---|---|---|

| Retail investors | Up to RM5,000 per issuer, max RM50,000 across all ECF platforms per 12-month period | General public, lowest barrier to entry |

| Angel investors | Up to RM500,000 across all ECF platforms per 12-month period | Must be accredited by MBAN |

| Sophisticated investors | No annual cap | High-net-worth individuals and institutions |

These limits were reaffirmed in the SC’s January 2025 revision of the RMO Guidelines.

How an ECF Campaign Works

- Choose a platform. Select an SC-registered ECF platform that fits your sector and target investor base.

- Submit for due diligence. The platform reviews your business documents, financials, and offer document. This typically takes 2 to 4 weeks.

- Launch the campaign. Your company profile, pitch, and investment terms go live on the platform. Campaigns usually run for 30 to 60 days.

- Investors commit funds. Retail, angel, and sophisticated investors review your pitch and invest. Some platforms require you to hit a minimum target before funds release.

- Close and receive funds. Once the campaign closes successfully, the platform processes share transfers and disburses funds to your company.

PSTX: Malaysia’s First ECF Secondary Market

One of the biggest drawbacks of ECF has always been liquidity. Once you invest, there was no easy way to sell your shares. That changed in July 2024 when pitchIN launched PSTX (pitchIN Secondary Trading Market), Malaysia’s first secondary trading market for ECF shares.

PSTX works like this: if you hold shares in a company that raised funds on pitchIN, you can list those shares for sale on the marketplace. Buyers browse available shares and create buy orders. The platform operates on a cash-upfront basis, and share prices are set by supply and demand. PSTX launched with 10 companies listed and has been adding more since.

For founders, this is a strong selling point when pitching to ECF investors: their capital is no longer locked in indefinitely. For investors, it creates a path to exit early-stage positions without waiting for an IPO or acquisition.

SC-Registered ECF Platforms in Malaysia (7 Active Platforms)

Malaysia currently has 10 SC-registered ECF platforms. Here are the seven most active ones for startup founders.

pitchIN

The most established ECF platform in Malaysia with over RM350 million raised, 18,000+ investors, and 184+ campaigns completed. pitchIN also operates PSTX (the secondary trading market) and offers Token Crowdfunding (TCF) for digital token projects. Hosts campaigns across technology, F&B, retail, and social enterprises. Approved as a NIMP CoSIF platform.

Ata Plus

An SC-registered platform that raised US$1.8 million across five successful campaigns in 2025, with investor interest expanding beyond tech startups into food security and agriculture. Provides end-to-end fundraising support including campaign strategy and compliance. Currently expanding into East Malaysia.

Leet Capital

Operated by 1337 Ventures, Leet Capital uses its accelerator network to source high-potential startups. Focuses on technology, health tech, real estate tech, and renewable energy. Minimum investment of RM15,000 positions it for experienced investors. Approved as a CoSIF platform.

MyStartr

One of Malaysia’s earlier ECF platforms, MyStartr hosts both equity and reward-based crowdfunding. The platform holds the record for Malaysia’s highest single ECF campaign: GoodMorning Global Group raised RM20 million from 1,046 investors.

Ethis

A Shariah-compliant ECF platform with licenses in Malaysia, Turkey, and Oman. Ethis focuses on ethical and socially responsible businesses. It also operates EthisX, a cross-border ethical private capital marketplace for global Shariah-compliant investments through Musharakah partnerships.

AMB Connect

A dedicated Islamic equity crowdfunding (ECF-i) platform registered with the SC. AMB Connect offers Shariah-compliant fundraising products tailored to different growth stages. Open to all Malaysian businesses regardless of state or industry.

Crowdo

One of the original SC-registered ECF operators. Crowdo is approved under the NIMP CoSIF programme, making it eligible to administer government co-investment campaigns alongside private investors in strategic NIMP 2030 sectors.

What Is Peer-to-Peer (P2P) Lending?

P2P lending (also called P2P financing) is a platform-based model where businesses borrow directly from individual investors, bypassing traditional banks. The platform handles credit assessment, fund collection, and repayment.

In Malaysia, P2P financing is regulated by the SC under the P2P Framework launched in 2016. By September 2024, over RM7.9 billion had been raised through 16 licensed P2P platforms. Malaysia’s alternative lending market is projected to grow from US$408 million in 2023 to US$1.03 billion by 2028 at a compound annual growth rate of 19%.

Key P2P Rules in Malaysia

- Regulated by the SC. Only licensed P2P operators can facilitate financing.

- Issuers (borrowers) can raise financing from as little as RM1,000.

- Investors can start with as little as RM50 on some platforms.

- Loan terms typically range from 1 to 24 months.

- Interest rates depend on the borrower’s credit profile and platform risk assessment. Investor returns generally range from 5% to 15% per annum.

How P2P Lending Works

- Register on a platform. Sign up as a borrower and submit your business documents and financial information.

- Credit assessment. The platform evaluates your creditworthiness using financial data, business track record, and sometimes alternative data sources.

- Campaign goes live. Your financing request is listed on the platform for investors to review and fund.

- Investors fund the loan. Multiple investors contribute to your financing, spreading risk across the pool.

- Receive funds. Once fully funded, the platform disburses the loan to your business account. This typically takes days to 2 weeks.

- Repay on schedule. You repay principal and interest per the agreed terms. Many platforms support both conventional and Shariah-compliant structures.

Licensed P2P Platforms in Malaysia (6 Active Platforms)

Malaysia has 16 SC-licensed P2P platforms. Here are six with strong track records for startup and SME financing.

Funding Societies (Modalku Ventures)

The largest P2P platform in ASEAN. Funding Societies offers term loans, invoice financing, and microloans for Malaysian SMEs. Uses machine learning and alternative data for risk assessment. Supports both conventional and Islamic financing. Historical default rate of approximately 3%.

MicroLEAP

Malaysia’s first P2P platform to offer both Shariah-compliant and conventional financing on the same platform. Also a partner in MTDC’s P2P Financing Programme for technology-based companies. Investors can start from as little as RM50.

Capsphere

Malaysia’s first asset-based P2P financing platform. Requires borrowers to put up collateral for each Investment Note, reducing investor risk. Default rate of approximately 1.5% as of December 2024. Also offers end-to-end Shariah-compliant financing.

CapBay

One of the lowest-risk P2P platforms in Malaysia with a default rate below 0.1% across over RM880 million in financing. Focuses on invoice financing and supply chain financing for SMEs.

Cofundr

A Shariah-compliant P2P crowd financing platform focused on micro, small, and medium enterprises (MSMEs). Connects qualified businesses with investors who want halal, risk-adjusted returns aligned with their values.

P2P Nusa Kapital

The world’s first regulated Shariah-compliant P2P platform. Based in Malaysia and focused on providing Islamic P2P financing that is free from riba (usury), maisir (gambling), and gharar (ambiguity).

ECF vs P2P Lending: Which Is Right for Your Startup?

| Equity Crowdfunding (ECF) | P2P Lending | |

|---|---|---|

| What you give up | Equity (ownership shares) | Interest on loan repayment |

| Repayment required? | No (equity, not debt) | Yes (principal + interest) |

| Typical amount | RM100K to RM10M+ | RM1K to RM2M |

| Best for | Growth capital, scaling, product development | Working capital, invoice financing, short-term needs |

| Timeline | 30 to 60 day campaigns + due diligence | Days to 2 weeks after approval |

| Investor relationship | Shareholders (long-term) | Lenders (until repayment complete) |

| Dilution | Yes | No |

| Shariah-compliant options | pitchIN, Ethis, AMB Connect | MicroLEAP, Capsphere, Nusa Kapital, Cofundr |

| Regulator | Securities Commission Malaysia | Securities Commission Malaysia |

Choose ECF If:

- You need larger growth capital and are willing to share equity

- You want to build a community of investor-advocates who champion your brand

- Your business has a story that resonates with retail investors

- You want market validation alongside funding

Choose P2P Lending If:

- You need working capital or bridge financing quickly

- You do not want to give up equity

- You have predictable cash flow to service loan repayments

- You need invoice financing or short-term operational funding

Combine Both Strategically

Many Malaysian startups use P2P lending for short-term operational needs while raising ECF or venture capital for growth. The two are not mutually exclusive. You can also layer government grants for startups in Malaysia (non-dilutive and non-repayable) as a foundation before pursuing either channel. If your startup operates in a NIMP 2030 manufacturing sector, the CoSIF co-investment programme amplifies both ECF and P2P raises even further.

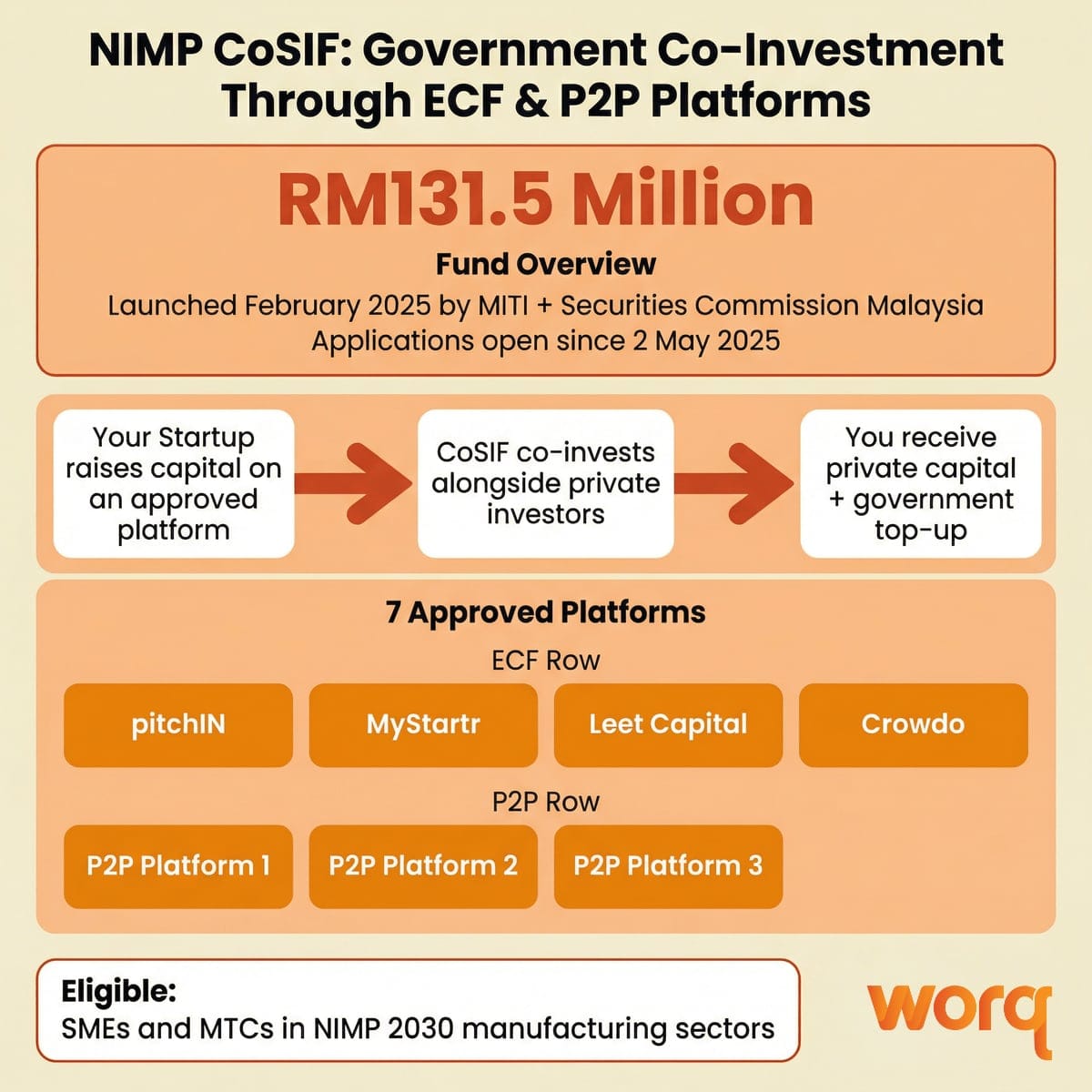

NIMP CoSIF: RM131.5 Million Government Co-Investment Through ECF and P2P

In February 2025, the Ministry of Investment, Trade and Industry (MITI) and the SC jointly launched the NIMP 2030 Strategic Co-Investment Fund (CoSIF) with an initial allocation of RM131.5 million. This is a government co-investment fund that puts money alongside private investors on ECF and P2P campaigns.

How it works: When your company runs a campaign on an approved platform and your business falls within NIMP 2030 eligible sectors, the government co-invests at a pre-determined ratio based on your sector. This effectively tops up the private capital you raise.

Seven platforms were approved to administer CoSIF campaigns: four ECF platforms (pitchIN, MyStartr, Leet Capital, and Crowdo) and three P2P platforms. Applications opened on 2 May 2025.

Who qualifies:

- SMEs and mid-tier companies (MTCs) in manufacturing or sectors aligned with the NIMP 2030 missions

- Must meet the CoSIF eligibility criteria (shareholders’ equity above RM2.5 million or 75+ full-time employees for manufacturing firms)

- Must raise funds through one of the seven approved platforms

This is the first time the Malaysian government has channeled co-investment capital directly through ECF and P2P platforms. If your startup operates in manufacturing, advanced materials, electrical and electronics, or other NIMP 2030 priority sectors, CoSIF can significantly increase the total capital raised from your campaign.

Shariah-Compliant ECF and P2P Options in Malaysia

Malaysia is one of the world’s largest Islamic finance markets, and its ECF and P2P infrastructure reflects this. Multiple platforms offer Shariah-compliant products for both founders raising capital and investors deploying it.

ECF platforms with Shariah-compliant campaigns:

- pitchIN offers Shariah-compliant ECF campaigns screened to exclude riba, maisir, and gharar

- Ethis is fully Shariah-compliant across all offerings, with cross-border reach

- AMB Connect is a dedicated Islamic ECF-i operator registered with the SC

P2P platforms with Shariah-compliant financing:

- MicroLEAP offers dual conventional and Islamic options on the same platform

- Capsphere runs end-to-end Shariah-compliant asset-based P2P financing

- P2P Nusa Kapital is the world’s first regulated Shariah-compliant P2P

- Cofundr focuses exclusively on halal P2P crowd financing

The SC supports a dual-finance model, allowing both conventional and Islamic ECF and P2P to coexist. Shariah-compliant financing uses Islamic contracts like Murabahah (cost-plus sale), Musharakah (partnership), Mudharabah (profit-sharing), and Wakalah (agency) instead of interest-based lending.

For founders, choosing a Shariah-compliant platform can open your campaign to a large pool of values-driven investors who specifically seek halal investment opportunities. These platforms are open to everyone, not just Muslim founders or investors.

How to Prepare for an ECF Campaign in 5 Steps

Running a successful ECF campaign takes more preparation than most founders expect. Here is what to have ready.

1. Business Documentation

- Company registration (SSM) and constitution

- Audited or management financial statements

- Business plan with clear growth strategy

- Cap table showing current ownership structure

2. Offer Document

The ECF platform will help you prepare an offer document that discloses the investment terms, risks, use of funds, and company financials. This is a regulatory requirement under the SC’s RMO Guidelines.

3. Pitch Materials

A strong pitch deck is the centrepiece of your ECF campaign. Beyond the deck, prepare:

- A pitch video (2 to 3 minutes)

- Clear campaign page with product screenshots or demos

- Financial projections with realistic assumptions

- Team bios with relevant experience

4. Marketing Plan

ECF campaigns need active promotion. Plan your outreach across social media, email lists, and personal networks. The most successful campaigns have a strong day-one push from the founder’s existing network, which builds momentum for organic investor interest.

5. Investor Communication Strategy

ECF investors expect updates. Plan for quarterly or monthly reporting on business progress, milestones, and financials. Platforms like pitchIN provide tools for this, but the content comes from you. If your shares trade on PSTX, regular updates also help maintain investor confidence and share liquidity.

How to Apply for P2P Lending in Malaysia

The P2P application process is faster and more straightforward than ECF:

- Choose a platform based on your financing needs (term loan, invoice financing, microloan, or Shariah-compliant options).

- Register and submit documents including SSM registration, bank statements (3 to 6 months), financial statements, and a business profile.

- Complete the credit assessment. The platform evaluates your risk profile and assigns a credit grade.

- Your financing request goes live. Investors review and fund your request.

- Receive funds once fully funded (typically within days to 2 weeks).

- Repay on schedule per the agreed terms. Both conventional and Islamic repayment structures are available.

Risks and Default Rates: What Founders Should Know

ECF Risks for Founders

- Dilution is permanent. Once you sell equity, those shareholders have rights. Plan your cap table carefully across multiple rounds.

- Campaign failure is public. If your ECF campaign does not hit its minimum target, that outcome is visible. Most platforms use an all-or-nothing model, so you receive nothing if the target is not met. Have a backup plan.

- Ongoing obligations. ECF shareholders may have information rights, and platforms may require quarterly or annual reporting.

P2P Risks for Founders

- Repayment is mandatory. Loans must be repaid regardless of business performance.

- Interest costs. Factor interest payments into your cash flow projections. Higher-risk borrowers face higher rates.

- Collateral requirements. Some platforms (like Capsphere) require asset-backed collateral for each Investment Note.

P2P Default Rates by Platform

Default rates vary across platforms and reflect differences in risk assessment, collateral policies, and borrower profiles:

| Platform | Default Rate | Notes |

|---|---|---|

| CapBay | <0.1% | Invoice and supply chain financing with strict screening |

| Capsphere | ~1.5% (Dec 2024) | Asset-backed collateral required for every note |

| Funding Societies | ~3% (historical) | Largest ASEAN P2P, broader borrower base |

| Industry range | 1% to 3.5% | Varies by platform, period, and financing type |

These numbers are self-reported by platforms. Default definitions can differ, so compare carefully. For founders borrowing through P2P, a lower platform default rate generally indicates stricter credit screening, which may mean longer approval times but also signals a more stable investor base willing to fund your request.

Where ECF and P2P Fit in Your Funding Strategy

ECF and P2P lending are two pieces of a larger funding puzzle. Most successful Malaysian startups combine multiple sources at different stages of growth.

A common pattern looks like this: start with a government grant to fund early development (non-dilutive, non-repayable), then use P2P lending for working capital as you grow, and raise an ECF round or VC investment when you are ready to scale. If your startup operates in a NIMP 2030 sector, apply for CoSIF to get government co-investment on top of your ECF or P2P raise.

At every stage, a strong pitch deck helps you communicate your story clearly, whether you are pitching to a crowd of ECF investors, a P2P platform’s credit team, or a venture capital firm.

For a complete overview of all 12 funding paths available to Malaysian founders, including bootstrapping, bank loans, angel investing, and more, read our pillar guide on startup funding in Malaysia.

Grow Your Startup at WORQ

Whether you are preparing an ECF campaign, running a lean operation funded by P2P lending, or stacking multiple funding sources, having the right workspace and community around you makes a real difference. At WORQ, we bring together founders, investors, and business professionals across Kuala Lumpur, creating a space where connections happen naturally.

From community events and networking sessions to quiet spaces for focused work, our coworking spaces are built for startups at every stage. Need a hot desk to get started or a private office for your growing team? We have flexible options that scale with you. Use our office space calculator to compare costs against a conventional office lease and find the right setup for your next stage of growth.

Frequently Asked Questions

1. Can foreigners invest in Malaysian ECF platforms?

Yes. The SC allows non-Malaysian investors to participate in ECF campaigns, though some platforms may have specific onboarding requirements for foreign investors. The three-tier investor classification (retail, angel, sophisticated) applies regardless of nationality. Foreign-owned companies can also raise funds through ECF, provided they are locally incorporated in Malaysia.

2. What happens if my ECF campaign does not reach its minimum target?

Most Malaysian ECF platforms operate on an all-or-nothing model. If your campaign does not hit the minimum funding target by the deadline, all committed funds are returned to investors and you receive nothing. Some platforms offer flexible funding where you keep what you raise, but this is less common. Always confirm the funding model with your platform before launching.

3. Do I need to be profitable to qualify for P2P lending?

Not necessarily. P2P platforms evaluate your overall creditworthiness, which includes revenue, cash flow, business track record, and financial health. Early-stage startups with limited revenue may find it harder to qualify, but some platforms specialise in micro-financing with lower thresholds. Having 3 to 6 months of bank statements and clean financial records strengthens your application.

4. What is Token Crowdfunding (TCF) and how is it different from ECF?

Token Crowdfunding is a newer SC-regulated fundraising channel where companies issue digital tokens instead of equity shares. Investors receive tokens that may represent utility rights, access, or other benefits tied to the business. Unlike ECF, TCF does not involve selling ownership shares. In Malaysia, pitchIN is currently the primary platform offering TCF alongside its ECF and PSTX services.

5. Are ECF and P2P returns taxable in Malaysia?

For P2P investors, interest income from P2P lending is subject to income tax. For ECF investors, capital gains from selling shares (including through PSTX) are generally not taxable for individuals, as Malaysia does not impose capital gains tax on shares of unlisted companies for individual investors as of 2026. Dividends from ECF investments follow standard tax treatment. Consult a tax professional for your specific situation.